When you’re just starting out in a product-based business, your main concern is getting product out the door so you can collect payment from customers. But as you scale up, you’ll need better inventory management.

Below we explore several benefits of small business inventory management and the methods experts recommend to best reap those benefits.

Why inventory management is important

Every small business knows the pain of not having enough cash flow, and inventory management has a significant impact on cash flow.

Stacey Kane, business development lead at EasyMerchant, says that if you buy too much stock and can’t sell it, you’re not only paying storage costs but also opportunity costs for revenue-generating products. In other words, the money and storage space you could have used for a better-selling product is tied up in a product that isn’t selling well.

“There’s also the risk of holding too much stock for too long and falling prey to, for example, price volatility,” explains Kane. With price volatility, if you buy a product at one price and hold onto it for too long, the price may go down. That difference in price means you’ll be selling stock at a lower margin than if you bought it at the lower price.

Another issue facing small businesses that don’t focus on inventory management: potential damage or reduced quality of stock. Kane notes that, as with any physical items, there are risks of degradation (such as rust), theft, fire damage, expiration, and so on. “The longer you hold items, the greater the chance of damage, so it’s important to keep stock constantly moving from storage to end user.”

Benefits of inventory management

Focusing on inventory management can help your small business

- Make better decisions. Giving the necessary time and attention to inventory management enables you to track sales, shipments, and production levels, according to David Mitroff, founder of Piedmont Avenue Consulting. “You can see which products are selling, where, and in what quantities. It’s also a great way to predict your entire supply and demand curve, and to adjust shipments and deliveries, or even production, to precisely meet your business needs.”

- Make financial plans. Inventory is the lifeblood of any product-based business, so finances naturally center on it. Keeping a close eye on inventory costs provides clarity for planning. And Sandra Hinshelwood, founder of Business Partner Magazine, says this can make or break a business. “I can’t emphasize this enough: The number one reason small companies fail is because of poor financial planning.”

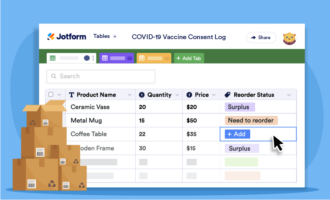

- Identify inventory anomalies. The movement of hundreds of products or more, day in and day out, can often leave gaps in inventory counts. These gaps negatively impact your bottom line and can be traced back to a number of causes, such as employee theft, inaccurate order picking, and more. “However, if you aren’t focusing on quality control with your inventory, you won’t be able to accurately identify the culprits,” says John Moss, CEO of English Blinds.

Best inventory management methods

To enjoy the benefits we discussed above, along with many others, inventory management experts recommend incorporating some of the inventory management methods below into your operations:

- First-in, first-out (FIFO). FIFO is a longstanding, simple inventory method that’s especially useful for perishable products. With FIFO, the oldest products are sold first. “FIFO is essential to avoiding product spoilage and associated costs,” explains Hinshelwood.

- Live inventory system. Keeping a constant pulse on stock levels is a must to keep costs from running amok. Kane recommends using a system that updates as you receive orders or otherwise change inventory counts. “As a small business, you may not be able to afford the best solutions, but even simple solutions can make a huge impact.”

- Traceability. It’s essential that your inventory management practices are traceable, whether they’re analog or digital. Moss explains that you should be able to easily identify who has handled, moved, sold, or returned inventory at any given time, which requires accurate reporting and record-keeping.

The methods you use will depend on the type of business you have, the type of products you store, your available storage space, and how fast your product counts change, among other variables.

Send Comment: